All major market segments saw seasonally adjusted prices that remained lower year over year in the first half of October, yet the declines have continued to be lower than earlier.

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) increased 0.3% from September in the first 15 days of October, according to the mid-month Manheim Used Vehicle Value Index released Oct. 17.

The index increased to 203.5, down 2.8% from October 2023. The seasonal adjustment reduced the results for the month. The non-adjusted price change in the first half of October fell 1.7% compared to September, and the unadjusted price was down 3.5% year over year. The average rise for the month of October is an increase of three-tenths of a point for seasonally adjusted values, so the current change is on target for the long-term trend expected in the early read of the month.

“We have maintained the belief that wholesale depreciation will be a bit muted in the future, and that’s what we are seeing in the first 15 days of October,” said Jeremy Robb, senior director of economic and insights at Cox Automotive, in a news release. “October typically brings the highest monthly depreciation rates for non-seasonally adjusted values of the year. While values have declined, they are down slightly less than we usually see now in the month.”

Over the last two weeks, the Manheim Market Report (MMR) prices in the Three-Year-Old Index declined by 1%, below the typical decline of 1.3% observed at this time of year. Over the first 15 days of October, MMR Retention, the average difference in price relative to current MMR, averaged 98.1%, indicating that valuation models are further away from market prices early in October. MMR Retention is down six-tenths of a point compared to the prior year at the beginning of October, and it is also a bit lower than the last two years.

The first-half average daily sales conversion rate of 56.6% was above the October 2019 daily average of 52.2%, but it has moved lower in the last two weeks due partly to slower business in regions impacted by recent hurricanes. The conversion rate has fallen almost three points from September 2024, indicating that buying demand has declined over the first half of October.

Wholesale Prices Range Below 2023 Levels

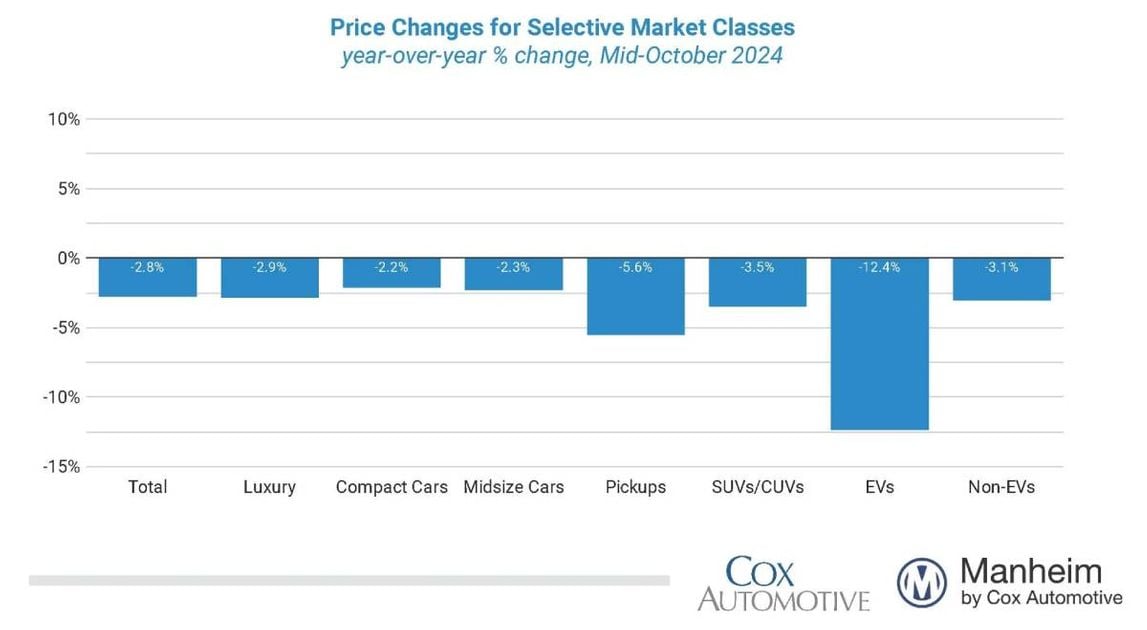

All major market segments saw seasonally adjusted prices that remained lower year over year in the first half of October, yet the declines have continued to be lower than earlier in the year. Compared to the industry’s year-over-year decline of 2.8%:

- Compact cars fell only 2.2%

- Midsize cars fell 2.3%.

- Luxury fell by 2.9%

- SUVs were down by 3.5%

- Pickups dropped 5.6% against last year

Segment results were mixed compared to the end of September. The overall industry rose by 0.3% compared to the prior month, with several segments showing better results.

By mid-month, compact cars increased by 1.4%, midsize cars rose by 1.2%, and pickups by 0.5%. On the other hand, SUVs were lower by 0.5%, and luxury fell the most, declining by 1.2%.

Electric vehicles (EVs) showed increasing depreciation so far this month and were down 12.4% against October 2023, while the non-EV segment decreased by 3.1% over the same period. Compared to September values, EVs declined 2% in the first half of October, while non-EVs were down 0.7%.

Wholesale Supply is Up in Mid-October

Leveraging Manheim sales and inventory data, estimated wholesale supply ended September at 27 days, up one day from the end of August and flat against September 2023, also at 27 days. Wholesale supply is relatively tighter for this time of year, running two days lower than the longer-term levels for this week. As of Oct. 15, wholesale supply increased by one day from the end of September, moving to 28 days, up one day versus last year.

Measures of Consumer Sentiment Showing Mixed Trends in October

- The initial October reading on Consumer Sentiment from the University of Michigan declined 1.7% to 68.9, disappointing as improvement was expected. Even with that decline, the index is up 8% yearly. The underlying views of both current conditions and future expectations declined. Expectations for inflation in one year increased to 2.9% from 2.7%, but expectations for inflation in five years fell to 3.0% from 3.1%. Consumers’ views of buying conditions for vehicles improved to the best level since April as views of interest rates improved.

- The daily consumer sentiment index from Morning Consult reflects more positive recent trends. The index increased 1.4% in September, extending a four-month upward trend, and now, as of the 15th, October is up 1.4%. That leaves the daily index up 10.8% yearly and at the highest level since spring 2021.

- The average price of unleaded gasoline is unchanged for the month as of Oct. 15 at $3.20 per gallon, which was down 11% year over year.